ALPHA BLEND

SYSTEMATIC BEHAVIOURAL FINANCE STRATEGIES

The firm’s partners have over 25 years of experience designing quantitative strategies for institutional clients.

Contact usCompany Profile

Absolute Return Strategies Ltd. (“ARS”) is a Fintech company specializing in Liquid Alternatives research and model building. The firm’s partners have over 25 years of experience designing quantitative strategies for institutional clients. ARS was formed in 2006 to create a new generation of Liquid Alt products for Citi under the brand “Alpha Blend”.

The company builds cutting edge quantitative models using Sentinel Software.

- All our software applications use Cloud-based infrastructure for robustness.

- Our quantitative behavioural analytics methodology is unique.

About Us

Investment Focus

- We design portfolios that seek positive returns independent of overall market direction.. This is distinct from traditional “relative return” investing, which aims simply to beat a benchmark.

- We are best known for our expertise in global markets, focusing on strategies with low correlation to equities and bonds.

Portfolio Roles

- Historically the firm has acted as advisor to Citi from 2006 to 2018 and to funds with absolute return objectives, such as the Silver Pepper Long/Short Emerging Markets Currency Fund, where our role was to manage the generation of Alpha.

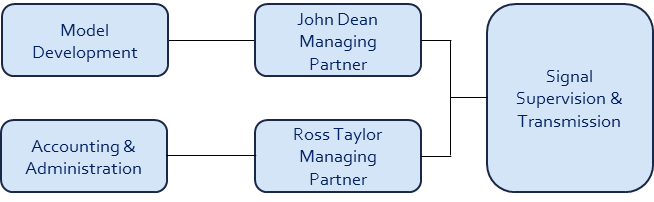

- The Managing Partners are John Dean, the Founder and CIO. and Ross Taylor COO. Both partners have substantial experience in the currency, equity and commodity markets.

Portfolio Roles

The Alpha Blend Global Macro portfolio is built around three core modules: Global FX, Equity, and Gold.

Our Objectives

Strategic Objectives

To be a leading Fintech company for institutional clients, defining the future of quantitative behavioural analytics in Liquid Alternatives.

We Incorporate both directional and mean reverting techniques to mitigate market risk and capture performance opportunities across a wide variety of asset classes

Further Objectives

To assist clients in generating low-risk Alpha in both “Risk On” and “Risk Off” market conditions this provides a zero-cost “Tail Risk” hedge.

Clients are responsible for executing trades based on our model signals using their own personnel.

Model Licensing

- Portfolio components in 3 modules, FX, Equity and Gold.

- The FX module contains a diverse mix of currencies……. G3 plus the most liquid Emerging Markets.

- Daily position and order updates are transmitted by email and/or voice

- No intraday trading.

- Simple approval process.

- A blend of Directional and Mean Reverting strategies.

- Effective in Risk On, Risk Neutral and Risk Off market conditions.

- Target clients are major corporate treasuries and family offices.

Management Team

John Dean

Founder and CIO. Former Managing Director at Donaldson Lufkin and Jenrette in Europe, leading Currency and Commodity activity and the Investment Management business. He has structured FX Alpha and Global Macro portfolios for over 30 years. He advised Swiss Banking Corporation on the launch of its FX Alpha fund (later the UBS Currency Fund) and served as Citibank’s exclusive FX Alpha Consultant from 2006 to 2018.

Ross Taylor

Managing Partner. Held senior roles at Bank Julius Baer, Daiwa Securities America, Bear Stearns and Natixis, spanning institutional FX and global markets. He led FX market making, execution and risk management across liquidity provision and flow trading. He pioneered FX prime brokerage and helped drive the shift to automated electronic trading, improving client connectivity, governance and scalable execution across platforms.

Our Product

We offer sophisticated Quantitative Trading Strategies built on a foundation of behavioural analytics and machine learning. Our primary function is to generate tactical trading signals across a diverse group of portfolio components, aiming to exploit short-to-medium-term market opportunities.

We have built our quantitative models using behavioural analytics with machine learning to understand how the participants, who generate positive and negative capital flows for each portfolio component, interact. Our parameter selection software runs on the AWS Supercomputer infrastructure. We build decision trees – each trained on a huge volume of historic price data for each component, to reveal repeating behavioural patterns.

Our models are tactical in nature as opposed to long-term econometric models. We use both directional and mean reverting models.

For each portfolio component we use separate long and short models. Each model comprises a parameter set for position entries and one for position exits so that there are four sets for each component.

All historic patterns are stored so that the code, which is run daily can search for and match them in the future.

Our proprietary code ranks parameter combinations by the Alpha generated. We select combinations which are part of a group with a flat kurtosis of returns, so that in the event of parameter shift the Alpha generated is not significantly degraded.

The simplest way to think about the philosophy behind the models is that if a market is trending… at some point there will be a reaction to the trend and at the end of that reaction there will be a move back in the direction of the trend. At each turning point a pattern of daily bars will be created.

The machine learning code can distinguish between significant patterns and non-significant patterns.

Research Methodology

The Foundations of Quantitative Behavioural Analytics

Quantitative behavioural analytics is an interdisciplinary field that combines data science, psychology, and statistical modelling to study and predict human behaviour through measurable, numerical data.

By leveraging large datasets using advanced computation allgorithms, and tools, this approach seeks to uncover patterns, trends, and insights into how large groups act and make decisions. In an era defined by digital transformation and the proliferation of data, quantitative behavioural analytics has emerged as a powerful tool in finance.

Quantitative Behavioural Analytics: Unveiling Human Behaviour Through Data

At its core, quantitative behavioural analytics relies on the systematic collection and analysis of behavioural data information that reflects what people do rather than what they say they do. Unlike qualitative methods, which focus on subjective experiences and narratives, quantitative approaches emphasize objectivity and scalability.

This is achieved by translating actions into numerical values that can be statistically analysed. The advent of super computing has supercharged this field.

The methodology typically involves several steps: data collection, preprocessing (cleaning and structuring the data), statistical analysis, and predictive modelling. Techniques such as machine learning are commonly employed to identify correlations.

Machine Learning

- We have written proprietary machine learning algorithms which run on the AWS Supercomputer infrastructure.

- The code generates entry and exit parameter sets which enable us to build long and short quantitative pattern matching models (locks & keys) for each portfolio component ie. combinations of entry and exit parameters.

- These historical patterns can be thought of as locks which need a matching key to “unlock”.

- All portfolio components exhibit either directional or mean reverting characteristics.

- Our machine learning algorithms have currently identified over 50 significant repeating patterns dependent on dominant cycle length and pattern complexity.

- The code typically ranks 2- 3 million combinations of entry and exit patterns for each portfolio component.

Investment Management & Partners

Investment Management

We have partnered with Record Asset Management to ensure our strategies are delivered within a robust institutional framework. Record Asset Management provides best-in-class signal execution and a mandate structuring platform, facilitating the professional and compliant delivery of our strategies to our clients.

Our Partnership with Record Asset Management

Record Asset Management is responsible for handling all of the critical operational aspects of this partnership. Their duties include negotiating investment management agreements, ensuring compliance with relevant regulations, executing trades, and managing all necessary accounting procedures.

For clients seeking a comprehensive, full-service investment management solution, this partnership with Record Asset Management offers the necessary structure and expertise. More information about our partner can be found on their website, Recordfg.com.

Record Financial Group Plc

(“Record”) Partnership

We have partnered with Record Financial Group Plc to deliver our strategies in an institutional format.

Absolute Return Strategies (“ARS”) Ltd

- Designing liquid alternate investment strategies for institutional clients for over 25 years.

- Experience includes:

- FX Alpha and Global Macro Portfolios for Swiss Banking Corporation (later became UBS Currency Fund)

- Exclusive FX Alpha consultant to Citibank (2006-2018)

Record Financial Group

- 40-year track record of managing derivatives and overlay solutions for institutional clients

- Sophisticated operational infrastructure and tailored reporting

- Deep, longstanding counterparty relationships ensuring best-execution and efficient implementation

Legal Statement

This Presentation is being provided to you on a confidential basis to provide preliminary information regarding the outcome of signals generated by the Absolute Return Strategies (“ARS”) Alpha Blend Global Macro and Global FX Strategies (“the Strategies”).

The performance information has been calculated on the basis of live model signals plus a factor for slippage and carry.

- No person has been authorized to make any statement concerning the Strategies other than as set forth in this Presentation and any such statements, if made, may not be relied upon. The information contained herein must be kept strictly confidential and may not be reproduced or redistributed in any format without the written approval of ARS.

- This material is for information purposes only and does not constitute a financial promotion, investment advice or an inducement or incitement to participate in any product, offering or investment. It does not constitute or form part of any offer to issue or sell, or any solicitation of any offer to subscribe or purchase any investment, nor shall it or the fact of its distribution form the basis of, or be relied on in connection with, any contract. No representation, warranty or undertaking, express or implied, is given as to the accuracy or completeness of the information or opinions contained in this presentation by ARS, its members or employees, and no liability is accepted by such persons for the accuracy or completeness of any such.

- Any summaries, illustrations, or projections contained in the presentation are not indicative that similar future performance can or will be achieved.

Get in Touch

rtaylor@alpha-blend.com

jdean@alpha-blend.com

ABSOLUTE RETURN STRATEGIES LTD